In August of 2016 the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2016-14 regarding the presentation of financial statements for nonprofit entities. The ASU is effective for annual financial statements issued for fiscal years beginning after December 15, 2017. For simplicity reasons FASSUB will be modified to make the new standard effective for all nonprofit owners with fiscal years ending December 31, 2018 and thereafter. The main provisions of this guidance as they pertain to REAC financial statement submissions are as follows:

- Reduces the classes of net assets from three to two. Nonprofits will report amounts for net assets with donor restrictions, and net assets without donor restrictions. Classification of net assets with temporary restrictions will be eliminated. The impact to multifamily reporting will generally be limited to those entities who were reporting Section 202/811 as temporarily restricted net assets. Owners will now be required to determine in which category of net assets amounts will be presented.

- Nonprofits may elect to present the cash flow on either the direct or indirect methods. HUD’s handbooks require the direct method. However, REAC has elected to exercise the option to eliminate the indirect reconciliation on the direct method cash flow. Accordingly, the REAC template will remain on the direct method, but the schedule will end after the determination of cash.

- For-Profit entities will retain the full direct method cash flow.

ASU 2016-14 also increases requirements for nonprofits to disclose expenses by both their natural and functional classifications in one of the following locations:

- On the face of the statement of activities

- In the notes to financial statements, or

- As a separate financial statement (data schedule)

REAC has determined that the FASSUB template will NOT be modified to collect this data. Rather, in REAC, the data will only be includable in a footnote. In general, there is no specific guidance issued on the classification. In multifamily, the majority of the costs are program services. The general decisions will reside in the administrative costs.

The full text of ASU 2016-14 can be found here.

A release date for the system modifications has not been determined yet but it is anticipated that this will occur before the end of the calendar year.

Proposed changes to Balance Sheet

Proposed changes to Profit & Loss

Proposed changes to Equity

Proposed changes to Cash Flow

{kind=link}

{kind=link}

{kind=link}

{kind=link}

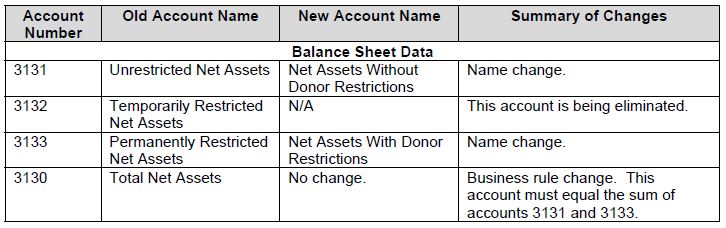

| Account Number | Old Account Name | New Account Name | Summary of Changes |

|

Balance Sheet Data |

|||

| 3131 | Unrestricted Net Assets | Net Assets Without Donor Restrictions | Name change. |

| 3132 | Temporarily Restricted Net Assets | N/A | This account is being eliminated. |

| 3133 | Permanently Restricted Net Assets | Net Assets With Donor Restrictions | Name change. |

| 3130 | Total Net Assets | No change. | Business rule change. This account must equal the sum of accounts 3131 and 3133. |

|

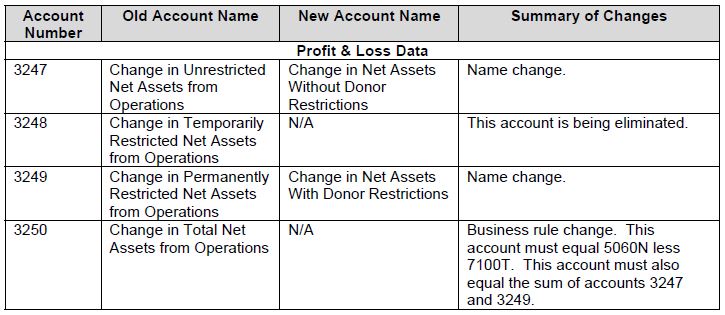

Profit & Loss Data |

|||

| 3247 | Change in Unrestricted Net Assets from Operations | Change in Net Assets Without Donor Restrictions | Name change. |

| 3248 | Change in Temporarily Restricted Net Assets from Operations | N/A | This account is being eliminated. |

| 3249 | Change in Permanently Restricted Net Assets from Operations | Change in Net Assets With Donor Restrictions | Name change. |

| 3250 | Change in Total Net Assets from Operations | N/A | Business rule change. This account must equal 5060N less 7100T. This account must also equal the sum of accounts 3247 and 3249. |

|

Equity Data |

|||

| S1100-060 | Previous Year Unrestricted Net Assets | Previous Year Net Assets Without Donor Restrictions | Name change. |

| 3247 | Change in Unrestricted Net Assets from Operations | Change in Net Assets Without Donor Restrictions | Name change. |

| S1100-065 | Other Changes in Unrestricted Net Assets | Other Changes in Net Assets Without Donor Restrictions | Name change. |

| 3131 | Unrestricted Net Assets | Net Assets Without Donor Restrictions | Name change. |

| S1100-070 | Previous Year Temporarily Restricted Net Assets | N/A | This account is being eliminated. |

| 3248 | Change in Temporarily Restricted Net Assets from Operations | N/A | This account is being eliminated. |

| S1100-075 | Other Changes in Temporarily Restricted Net Assets | N/A | This account is being eliminated. |

| 3132 | Temporarily Restricted Net Assets | N/A | This account is being eliminated. |

| S1100-080 | Previous Year Permanently Restricted Net Assets | Previous Year Net Assets With Donor Restrictions | Name change. |

| 3249 | Change in Permanently Restricted Net Assets from Operations | Change in Net Assets With Donor Restrictions | Name change. |

| S1100-085 | Other Changes in Permanently Restricted Net Assets | Other Changes in Net Assets With Donor Restrictions | Name change. |

| 3133 | Permanently Restricted Net Assets | Net Assets With Donor Restrictions | Name change. |

| S1100-050 | Previous Year Total Net Assets | N/A | Business rule change. This account must equal the sum of accounts S1100-060 and

S1100-080. |

| 3250 | Change in Total Net Assets from Operations | N/A | Business rule change. This account must equal 5060N less 7100T. This account must also equal the sum of accounts 3247 and 3249. |

| S1100-055 | Other Changes in Total Net Assets | N/A | Business rule change. This account must equal the sum of accounts S1100-065 and

S1100-085. |

| 3130 | Total Net Assets | N/A | Business rule change. This account must equal the sum of accounts 3131 and 3133. |

|

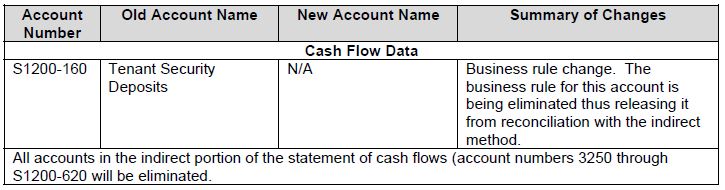

Cash Flow Data |

|||

| S1200-160 | Tenant Security Deposits | N/A | Business rule change. The business rule for this account is being eliminated thus releasing it from reconciliation with the indirect method. |

|

All accounts in the indirect portion of the statement of cash flows (account numbers 3250 through S1200-620) will be eliminated. |

|||